作者 | 格隆

数据支持 | 勾股大数据(www.gogudata.com)

谈股论金,侃天侃地,大家好,我是格隆。

大家都知道,我是做宏观研究的,而且主要用数据说话。但遗憾的是,过去三年里,我的宏观模型里需要跟踪的三百来个数据,有多达170多个,消失了,根本拿不到了。这也是我最近比较少说话的原因之一。

但饶是如此,我的数据团队依然开发了很多性感的新维度另类数据,我们大致可以从这些另类数据里窥探到我们整个经济的温度与时代的脉搏。

我一直强调,我们所赚的所有的钱,都是一个时代大趋势的钱。

所谓命运,命,就是你出生的家庭和父母,运,就是你所在的时代和经济大周期。如果不看清时代,做不到人间清醒,你的生活很大概率会随波逐流,越来越走向逼仄、焦困。

今天格隆带大家从两个非常有意思的视角,来窥视我们经济运行的现状与未来走向。

什么视角呢?“食”和“色”。

《孟子·告子》有言“食色,性也”。什么意思呢?也就是说喜好美食和美色,是人的动物本性,是人类最底层、最基本的欲望与需求。

人是从什么时候真正衰老的呢?是从他(她)没有性欲望和性需求开始的。如果人群连食和色这两个最底层欲望都放弃了,那就绝对是苟活于世,哀莫大于心死,“禽兽不如”了。

我们数据团队的数据显示,中国社会的“食萧条”、“性萧条”特征已非常明显,且程度在不断加深、加重。

我们先来看看“食萧条”。

2025年1-4月,中国实现餐饮总收入1.82万亿元,同比增长4.8%。看起来还在微幅增长,但这一增速,是除疫情的2020年和2022年这两年之外的历史最低值,甚至比同期的GDP增速还低了一大截。

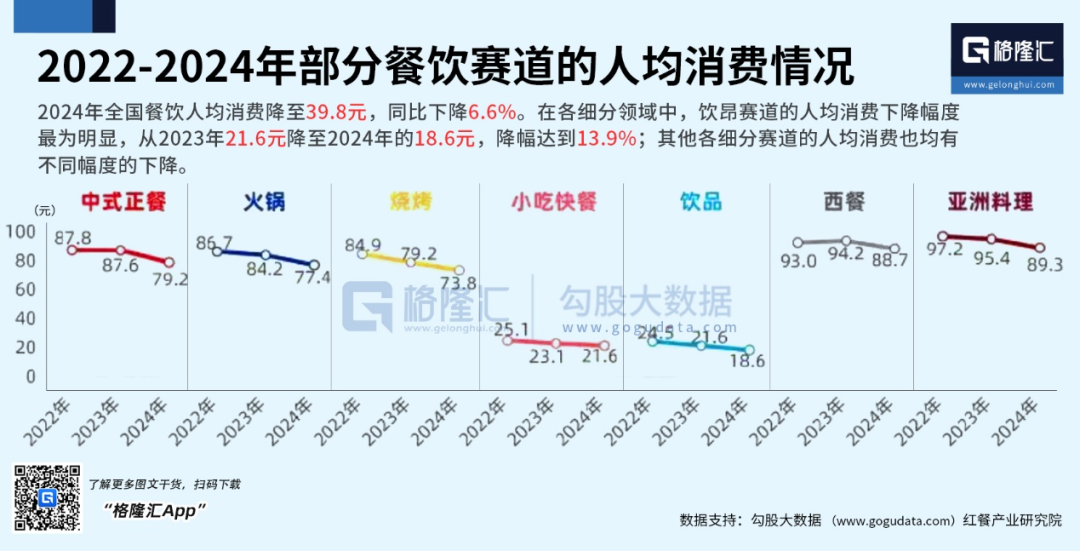

从人均消费数据来看,数据更是糟心。2022-2024年,中国餐饮人均消费值持续下滑。大家看看下面我们的数据图一。数据显示,2024年,全国餐饮人均消费已降至39.8元,这是有这个统计数据以来的历史最低值。

从细分项上看,无论饮品类,还是中式正餐、火锅类、烧烤类、快餐,乃至西餐、料理,全军覆没,没有一个不下降的。最为显著的是饮品类,从2023年的21.6元下降到2024年的18.6元,大幅下降了13.9%。这或许就是单品价格低到令人发指的蜜雪冰城能够火的原因。

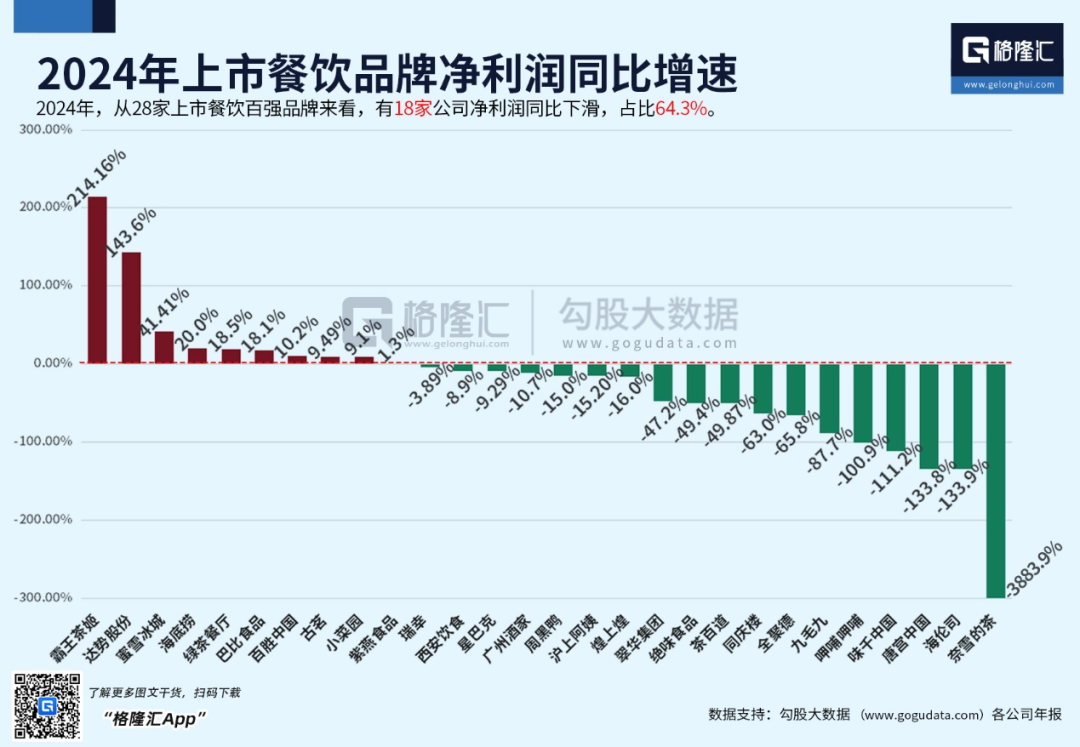

体现到行业利润上,餐饮利润大幅下滑。2024年,28家上市餐饮百强品牌中,有6家亏损,18家净利润同比增速下滑,亏损+利润增速下降的企业占比达到了恐怖的86%。

这些大型上市餐饮公司的利润都在大幅下降,更不用说中小型餐馆了,迎接他们的不是亏损,而是整个餐饮行业前所未有的倒闭潮。

大家看看下面这个数据,很令人揪心。从图中我们可以清晰看到,2018年是个拐点。我们不知道2018年发生了什么,但数据显示,2017年以及之前,我们每年倒闭的餐饮企业只有10万家上下。但仅仅7年后,也就是2024年,当年餐饮企业倒闭数量达到了230万家,倒闭餐饮企业数量创下历史新高,是2017年倒闭数量的14倍,比上一年也就是2023年的135.9万家,也增加了近百万家,增幅高达69%,显示形势其实是在进一步恶化。

看完了“食萧条”,我们再来看看更严重的“性萧条”。

还是用数据说话:

2022年,北京大学和复旦大学共同发起了“中国人私生活质量调查”,6828份有效问卷显示:中国年轻一代的性活跃度呈严重下降趋势,超过一半的95后性生活频率低于每周一次。

这是什么概念呢?这个性生活频率,比80后甚至70后的中老年人,还要低。

如果你觉得上面抽样调查的样本数还不够大,你再看看下面几个数据,就知道我们的性萧条有多严重了。

比如,结婚人数大幅减少。2025年第一季度,我国结婚人数降至181万对,较去年同期减少15.9万对。除去疫情特殊时期,今年一季度的结婚人数,果断创下了历史新低。

再看看相关性用品数据。

白云山年报显示,国产伟哥代表金戈的销量,从2023年的1亿片,大幅降到8785万片,日均销量则从27.7万片降到24万片,同比下降13.2%。销售额呢?从12.9亿元下降到了10.3亿元,同比降幅为20.2%。

这意味着什么?意味着用伟哥的那个群体,去年有高达13%的人,停止了他们的性生活。

不仅是国产品牌,进口原版品牌万艾可(Viagra)在2024年的销量同比也下降了7.7%,金戈和万艾可作为占据国内市场份额92.9%的两大主力品牌,他们的销量双双遇冷,足以说明整个市场的萧条程度。

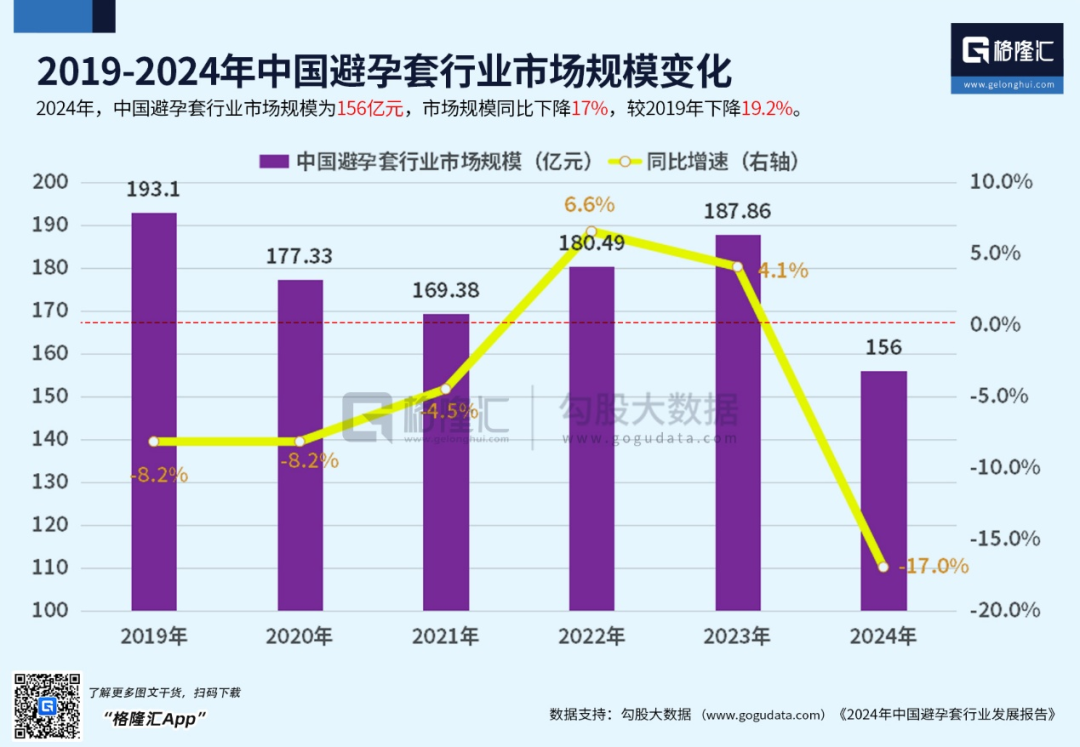

如果说伟哥还只是部分群体使用,那避孕套数据,就会更有说服力。

格隆直接上数据:2024年中国避孕套市场规模156亿元。这是什么概念呢?2023年避孕套卖了187.86亿元。2024年足足下降了17%——这个数据,比伟哥,更加“萧条”。

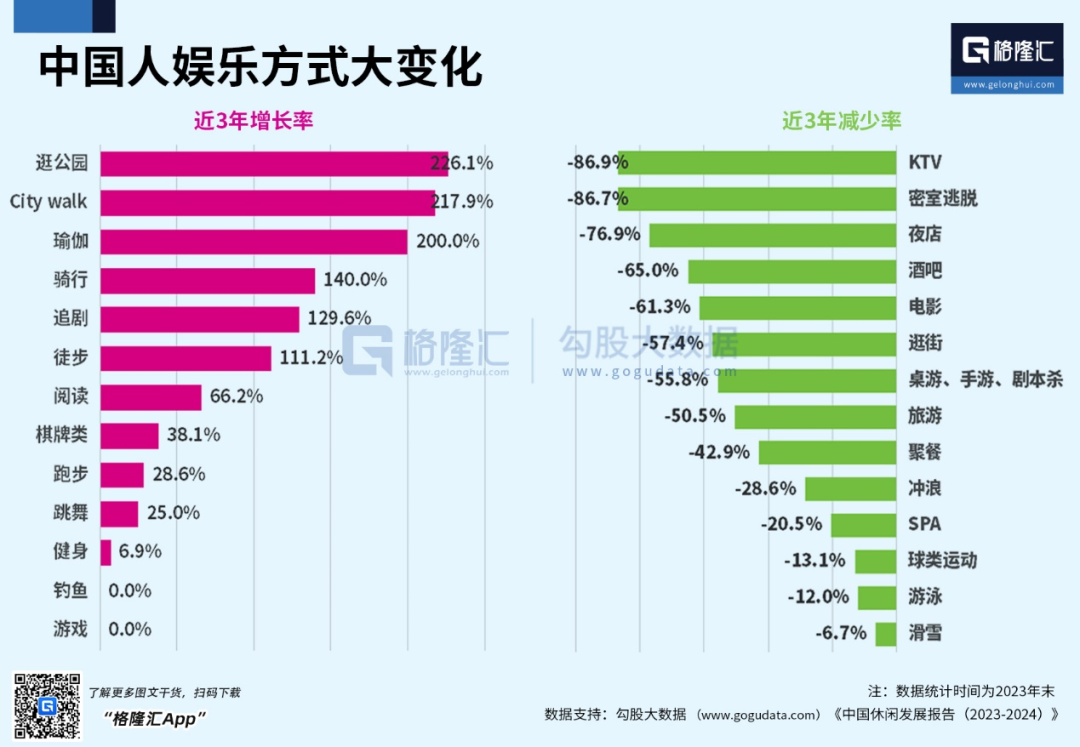

更不用说性需求衍生的暧昧消费了,比如酒吧、KTV、夜店等社交消费也在大幅降温。过去三年,KTV消费降幅高达86.9%,夜店娱乐降幅也高达76.9%,酒吧消费也下降了65%。

大家干嘛去了呢?

看看下面的数据图,大家去逛公园、练瑜伽、徒步和跑步去了——这些都只需要动动腿,不需要动荷尔蒙。

“饮食男女,人之大欲存焉”。心理学家弗洛伊德认为:“人类的一切痛苦,都是因为性欲得不到满足。”性是人类的根本欲望,甚至大部分经济活动都来源于性的驱动。但当前一系列反人类本性的经济数据充分表明,大家都在压抑自己最最基本的生理欲望,没有人再向往甚至不屑于“今夕何夕兮,搴舟中流。今日何日兮,得与王子同舟”的美好,我们的社会正在加速滑向一个低欲望社会——性,美食,更罔谈赚钱欲望、创业欲望、旅游欲望、消费欲望。

低欲望社会,会带来什么深远影响?

格隆复盘过这个星球上几乎所有核心经济体的历史,我发现一个规律:经济萧条,其实并不可怕,周期而已。比经济萧条更可怕的,是全社会的低欲望,它会把一个社会拖入一个欲罢不能的长期泥沼。

太阳底下没有新鲜事,看看和我们经济崛起路径极度类似的邻国日本就好了。

上世纪90年代,在日本经济泡沫破裂带来的剧痛中出生的“平成废宅”,少年时代亲历着日本股市和房价暴跌带来的动荡,在大学生就业率仅有56%的年代里,平成青年直接“躺平”。

他们不结婚,日本18-34岁年轻男性中单身比例常年维持64%左右;不生孩子,日本出生人口数从1994年之后就开始直线下滑,到2009年之后日本就进入了人口负增长时代;不买房子,根据日本政府统计,从1983年到2008年的25年间,30岁至39岁的持房率从53.3%降至39%,30岁以下的持房率也从17.9%降至7.5%。

低欲望社会,带来的结果是什么呢?

最直接的影响是消费,日本消费由盛转衰,泡沫破裂前的1985-1990年,日本消费平均增速为4.6%,但在泡沫经济破裂后,日本消费增速迅速回落,1991-2010年平均增速仅为0.92%。需求不振,物价持续走低,日本GDP平减指数从1990年开始下降,1995到2013年经历了19年的负增长,日本经济进入通缩螺旋,1990-2010,GDP增速只有可怜的0.92%,日本经济陷入“失落的二十年”。

在失落的时代,日本政府也在大力挽救经济危机。

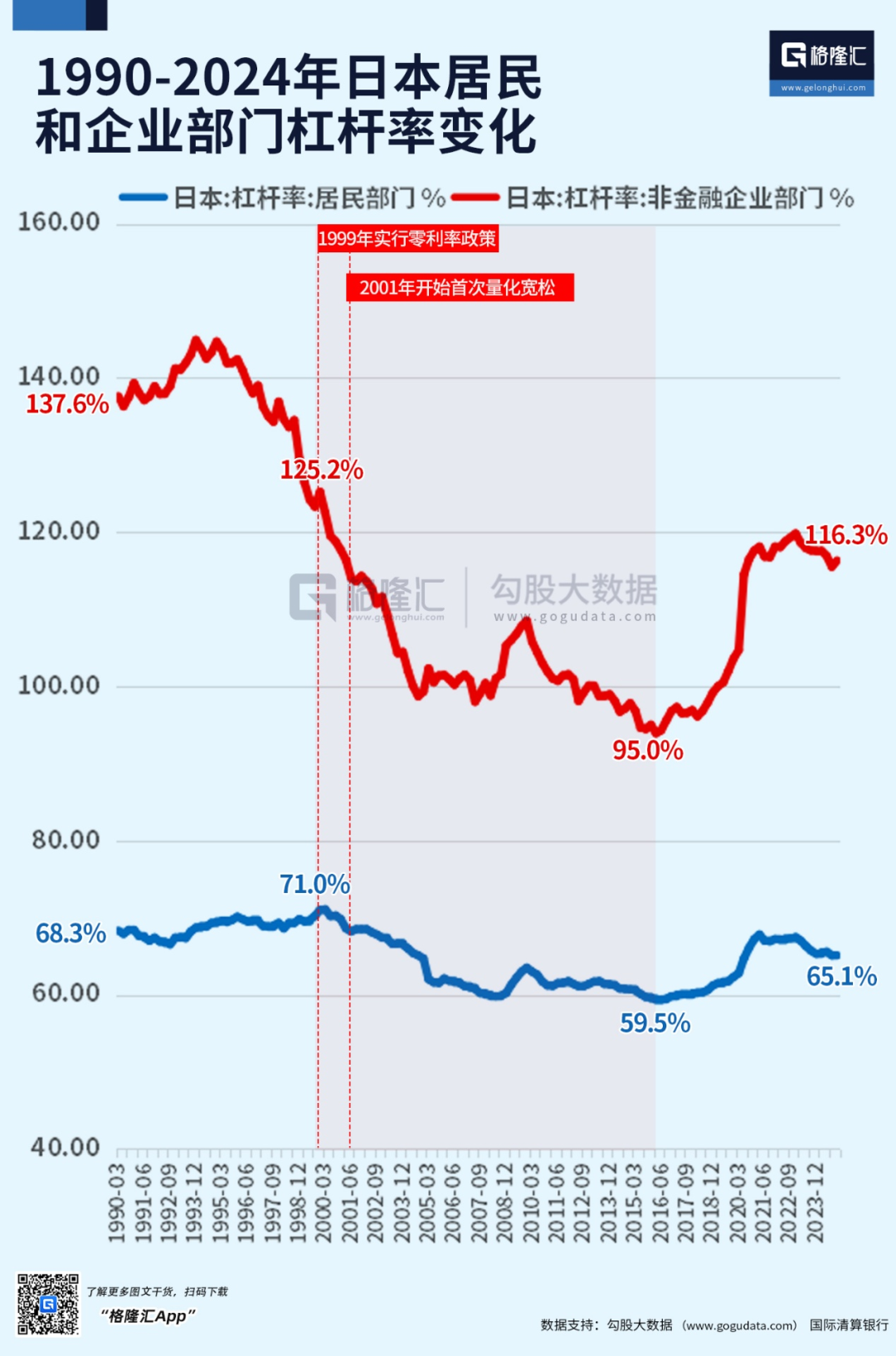

为了刺激经济,1999年2月,日本政府就开始实行零利率政策,直到2024年5月才结束零利率政策,并且于2001年3月开始首次量化宽松,并且在2013年“安倍经济学”中得到强化。

可是这些极度宽松的货币政策并没有快速扭转日本居民和企业部门的去杠杆进程。日本央行1999年就把利率降到0,可是2000年到2015年,这15年的时间,日本企业和居民仍旧在加速去杠杆。1999年到2015年,日本企业部门杠杆率从125.2%降至低点98%,居民部门杠杆率则从71%一路降至59.5%。

要知道,利率下降,意味着借款成本降低。在一个健康的经济体中,借贷成本降低,会刺激信贷需求,增加居民消费支出,进而提振总需求,带动经济回暖。

但由于日本社会的低欲望,无论利率降得多低,他们也不结婚,不贷款消费,不买车不买房,这就使得日本政府在2000年前后施行的货币政策完全失效。

从数据上可以清晰看出,日本经济失去的20年,其实前十年后核心经济数据已经触底,按道理经济就应该逐步爬出泥沼了。但低欲望社会,让日本经济在2000年之后,硬生生在泥潭中多挣扎了10年之久。

历史不会简单的重复,但总是押着相似的韵脚。回到当下的中国,再怎么高估食色双萧条、低欲望社会对我们经济的冲击,都不过分。

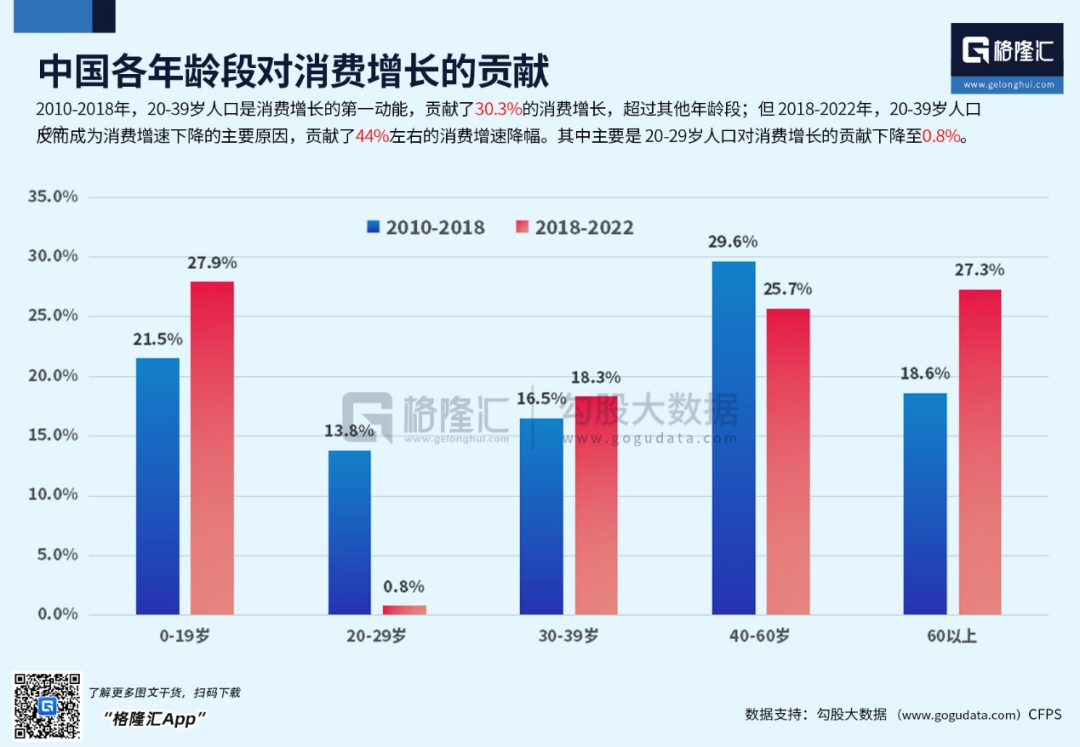

大家看看下面的数据图。我们的消费增速,在2015-2019年,平均水平为9.7%,但2020-2024年,这一增速则大幅降至3.8%。最糟糕是我们的年轻群体在大大降低自己的消费水平。

大家看一下下面这张图:2010-2018年,社零消费年复合增速为12%,2018-2022年年均增速降到了6.1%,而从不同年龄段的消费情况来看,20-39岁人口是消费增速下降的主要原因,贡献了44%左右的消费增速降幅。

居民部门的信贷需求也在发生剧烈变化。我们仍以2018年这个拐点年做比较基准。2018年5月,居民部门新增贷款的信贷占比为53.4%;7年后的今天,2025年5月,居民部门信贷需求占比是多数呢?

8.7%。

7年时间,居民部门信贷需求发生剧变,占比从53.4%下降至8.7%,大幅下滑83.7%。

与之对应的是,2025年5月,我们的总的新增信贷只有6200亿,同比下降了34.7%。

性需求都放弃了,谁还会去举债上杠杆呢?

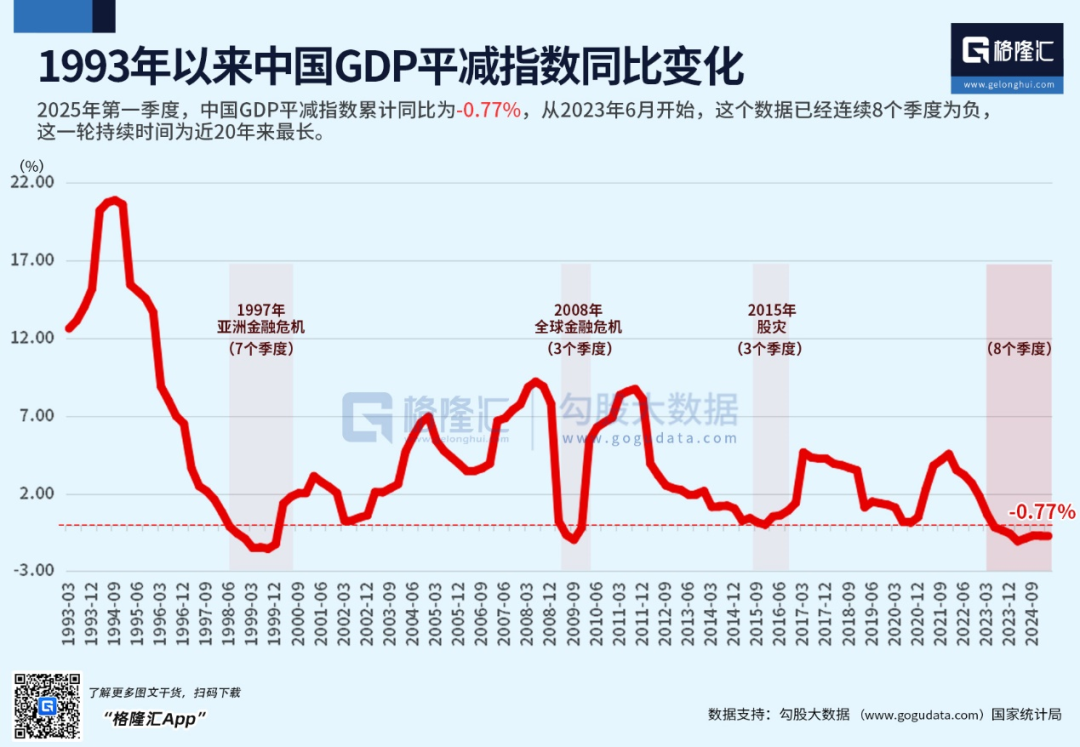

一个经济体的支出来自于两部分,货币和信用,信贷是经济中最重要的组成部分,获得信贷,增加支出,驱动经济上行。信贷需求大幅降低,消费不振,结果就是经济通缩。我们的GDP平减指数已经连续8个季度为负,这是该项数据有统计以来最长时期的连续负增长。

那是不是说经济下行,人们就一定节制消费,甚至节欲呢?

当然不是。

看看经济也饱受疫情冲击的美国居民消费信贷的数据:

数据显示,美国人正以惊人的速度在举债消费:2025年4月,美国消费者信贷增加了178亿美元,比上月增加了一倍还要多。尤其市场关注的学生贷款,飙升到了108万亿美元的历史新高——说实话,中美这两个国家都很奇葩。两国人民都在做自己最擅长的事情:美国哪怕十年期国债收益率一度被推高到4.6%了,他们的人还在可着劲消费。而中国十年期国债收益率被干到了只有1.5%,很多银行存款都不给利息了,中国人还是在拼命把钱存起来,而不是用于消费。

说明什么?说明食色的萧条,从来不是禁欲主义的胜利,而是人们在生存重压、未来无着之下生物本能的溃败。

如果我们不高度正视和扭转这个现实,甚至自我掩饰,低欲望社会会把我们的经济调整周期人为再拉长20年,也就是一代人的时间,绝非危言耸听。

破局的关键,不在于多建一些情趣酒店或是开放性消费场所,也不在于往人们口袋里多发一点消费券或者一些宏大叙事的宣发,而是实实在在给予人们,尤其是年轻人更多的希望:这个希望,或是兜底的社保,或是不板结、更灵活的社会阶层晋身机制,或是更市场化、更开放包容、更公平的财富创造与财富分配机制。

大仲马在《基督山伯爵》的结尾是这样写的:“人类的一切智慧就包含在四个字里面——“等待”和“希望”!”

一个人的一生可以没有很多东西,唯独不能没有希望。家与国,皆是如此。

我是格隆。关注我,做一个清醒的人。虽然有时候太清醒了也会很痛苦,但我向你保证,稀里糊涂随波逐流的代价,一定会更大。(全文完)

格隆汇声明:文中观点均来自原作者,不代表格隆汇观点及立场。特别提醒,投资决策需建立在独立思考之上,本文内容仅供参考,不作为任何实际操作建议,交易风险自担。

转自: 格隆 https://mp.weixin.qq.com/s/jH3RfqL1L-Z91OVuBsP6XQ